2024 Farmland Values

2024 Farmland Values

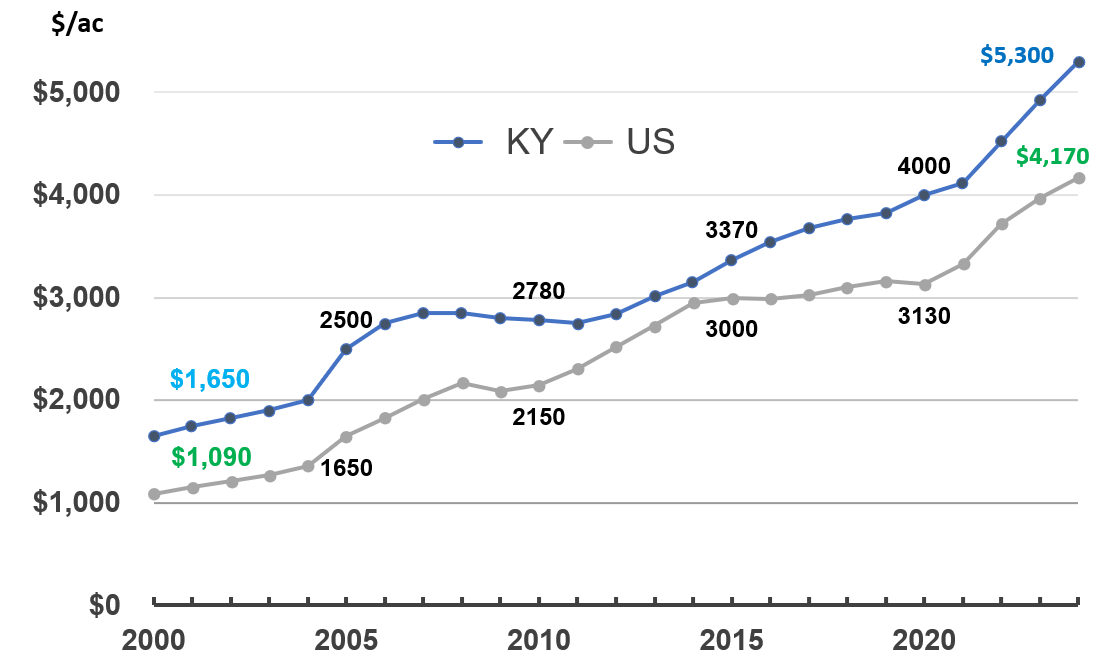

According to USDA estimates from their annual Land Values Summary, Kentucky’s average Farm Real Estate Values increased 7.5% in 2024 to $5,300/acre, up from $4,930 in 2023. Figure 1 is a comparison of Kentucky land values with the national trend since 2000. Kentucky’s values trend generally with national values, exceeding the national average while trailing most Midwestern states. Kentucky’s average Cropland Value increased from $5,720/ac to $6,220/ac (8.7%) while Kentucky’s Pastureland Value was up 5.6% from $3,570 to $3,770/ac.

Each August the USDA releases the results of their annual survey of farmland values. The survey includes data from approximately 9,000 tracts of land of about one square mile each across the continental United States. The survey takes place in early June and reports the separate values of cropland and pastureland, and the value of all land and buildings to arrive at an average “farm real estate value.” The average farm real estate value is the widely reported farmland value. This year the national average is $4,170/acre, an increase of 5.0% from 2023. This is less than the 7.4% increase reported in 2023. State level values are also reported. The complete 2024 Land Values Summary is available from the National Agricultural Statistics Service of USDA.

Nationally, average cropland values increased 4.7% to $5,570/ac from $5,320 a year earlier. US pastureland value increased 5.2% to $1,830/ac. These are the June survey averages. They do not represent the per acre prices for specific tracts nor are they an average of sale values. The USDA averages are a broad indicator of changes in land values.

Land values are determined by a number of factors including productivity, local demand, and other quality or location attributes. Simply put, land prices are set locally. Development pressure, for example, can cause land value increases far above agricultural values. Another widely observed demand factor influencing farmland values in Kentucky is the purchase of land (often seen only on an internet site) by out-of-state buyers who see Kentucky farmland as a bargain compared to high real estate price states in, for instance, California, Illinois, or New Jersey.

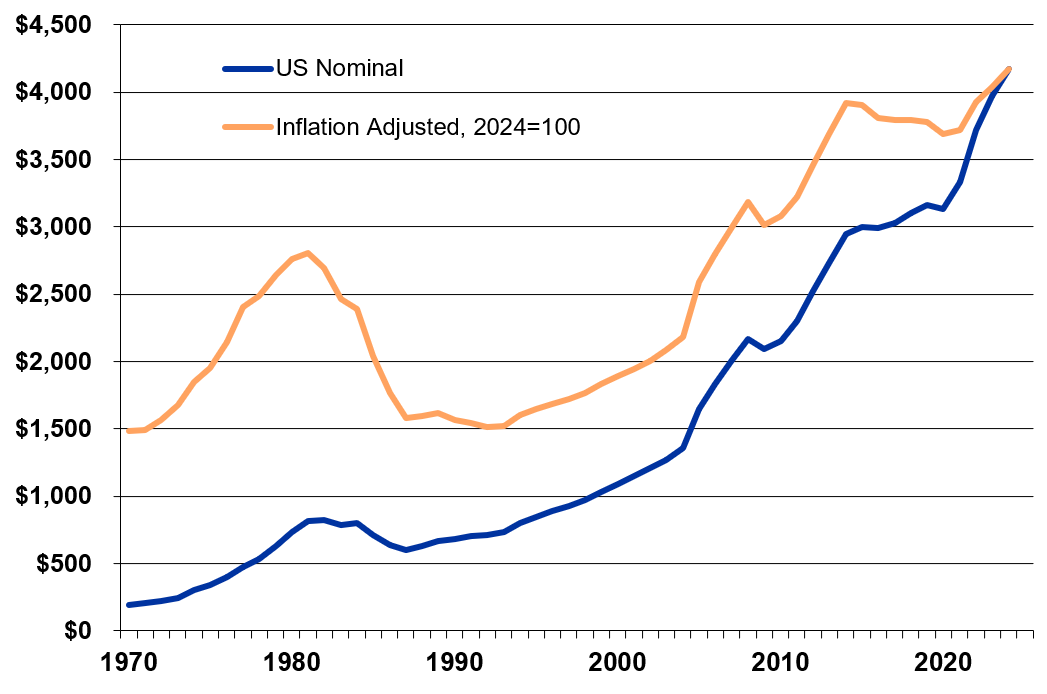

Land value changes are widely reported in the farm literature, usually in the format of Figure 2 without an inflation adjustment. This graphic captures data between 1970 when farm real estate was valued at $196/acre and 2024 with its $4,170/ac in nominal dollars (actual observed values). Figure 2 includes inflation adjusted values as well. The 1970 inflation adjusted value (also called real value) was $1,406/ac in today’s dollars. In real terms, land values peaked at $2,803/ac in 1981 prior to the ag financial crisis of the 80s. Real values did not reach that level again until 2006.

In nominal terms land values have increased more than 2,000% in the last 55 years ($196/ac to $4,170/ac). In real (inflation adjusted terms) land values have increased 181% over the same period ($1,486 to $4,170/ac) even when we consider the twenty-five years it took to recover from the crisis years of the 80s. Land values have beat inflation over this period by an average of 2.1%/yr with some pretty impressive swings. When land prices jumped 21.3% in 2005, that was 19.2% above inflation. However, an 11.0% decline in land values in 1985, coupled with a 4.4% inflation rate saw real land prices fall by 15.4%. Land value increases failed to exceed overall inflation in sixteen of those fifty-five years with most of those occurring during the farm crisis of the 1980s when land values were falling at the same time inflation was high.

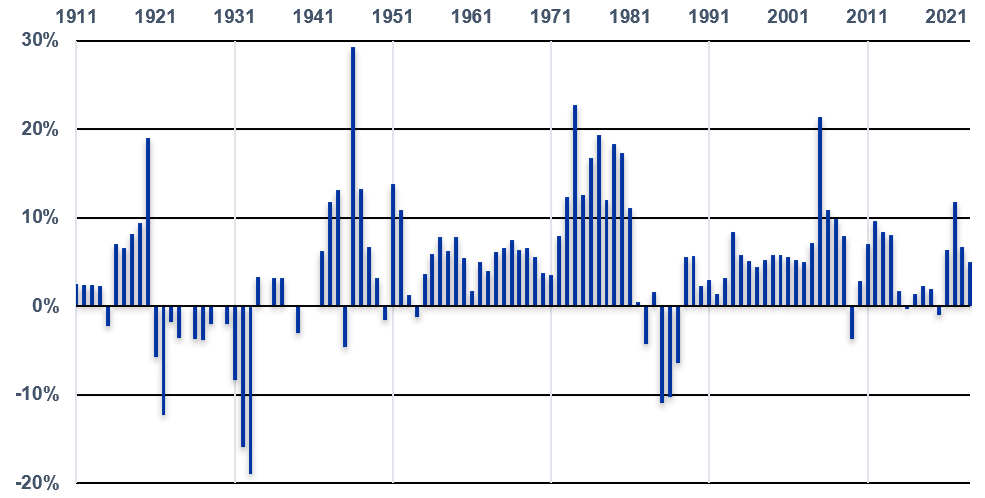

The year-to-year percentage changes in nominal (observed) values are shown in Figures 3. Farmland values are obviously affected by swings in commodity prices and farm profitability. The postwar period of the 50s, 60s, and 70s led to a notion that land values would always increase. They 80s laid waste to that notion. Land values have increased over the long run, but not without some hiccups.

Land, as an investment, shows a modest 2.1% average growth rate after accounting for inflation. However, land is a productive asset that does not depreciate and generates income in production or rent. Real estate represents 84% of the farm sector balance sheet assets, so changes in land values are important. Land is an investment with changes in value often determined by local conditions and farm profitability. It is a tangible asset, and many of us like to walk on our investments.

Figure 1. Kentucky & U.S. Farm Real Estate Values ($/acre) 2000-2024

Figure 2. United States Farm Real Estate Values ($/acre) 1970-2024

Figure 3. Annual Percentage Change in U.S. Land Values, 1911-2024

Recommended Citation Format:

Isaacs, S. "2024 Farmland Values." Economic and Policy Update (24):8, Department of Agricultural Economics, University of Kentucky, August 29, 2024.

Author(s) Contact Information: